Hearables… Discover why this often overlooked sector of wearable technology may represent the next multi-billion dollar industry.

Report Author: Nick Hunn, Wifore Consulting. London, 2016

This report was prepared for the purposes of providing Nuheara Ltd, a public company listed on the Australian Security Exchange (ASX), with industry research into its addressable (hearables) market.

All effort has been made by WiFore Consulting to ensure that information in this report is accurate and appropriate at the time of writing. Conclusions, and assumptions attached to those conclusions, are based on WiFore Consulting’s investigations and analyses of the facts WiFore Consulting is of the opinion that the conclusions and underlying assumptions are reasonable.

Source Documentation

All public information contained in this document can be sourced backed to, and verified against, the following article: “The Market for Smart Wearable Technology – A Consume Centric Approach” dated February 2015 by Nick Hunn, WiFore Consulting. All references in that article apply equally to this report.

An Introduction to Hearables

2015 was the year in which wearable technology finally started to make the move from niche to mainstream. Interest has focused on a few favorites – Fitbit and its successful IPO, Pebble’s emergence as an apparently credible smart watch company, and above all the eventual availability of the Apple Watch. These three persuaded the media that wearables had arrived. As with all technologies climbing the slope of the hype curve, that promise is somewhat exaggerated. The fact is that much of what is being offered is still an experiment, but an experiment that is growing in scale. As with Google’s Glass, Apple’s watch – the current poster child for wearables, is itself an experiment, albeit one which will benefit from having millions of guinea pigs to provide data to shape the future of the wearable experience. It has also served to dampen competition, as the wearables industry and the media hype behind it has paused to take breath.

Behind the excitement, little has been done to examine the many different sectors of wearables. The three above have all focused attention on the wrist, either as the site for fitness bands or for new, connected watches. From an industry perspective, the wrist has several advantages. It is a piece of “skin estate” which is increasingly available, as watch wearing has declined with the growing use of mobile phones, and more importantly, it provides a fair amount of space for cramming in technology and batteries.

That latter point is often missed, but it’s an important one. Despite the advances in miniaturizing technology, there are still practical limitations in what you can squeeze into a small space. There are even greater limitations on providing enough power from current battery technology. These constraints affect almost all wearable devices, which attempt to cram sensors, transducers, processing, display and batteries into a volume typically less than a tenth that of the smallest mobile phone. It means that many of the more exotic concepts in wearables, whether that be implantable devices or anything with a cellular modem are potentially still a decade away.

Whilst the wrist is attractive to the consumer electronics industry, it is not a new challenge. Watch makers have been innovating with watches for the last decade in an effort to counter the fall in sales. Wireless connectivity has been added, as have sensors and other features. None have stopped the overall decline. Even if you add in the recent success of Pebble and Apple, overall watch sales continue to fall. That may change, but we are only at the beginning of the watch experiment.

In contrast, a second area of wearable technology has been remarkably successful, but largely overlooked. That is the area of hearables – devices which are worn in or on the ear. The market has separated into two distinct streams.

The first is ear buds and headsets, largely growing from the attraction of personal music players, starting with the Sony Walkman and boosted by the iPod and the subsequent improvement in delivery of streamed music. Although the bulk of it still consists of sub US$1, wired earbuds, the top end segment of wireless headsets and earbuds, often utilizing advanced DSP (digital signal processing) technology for noise cancelling has recently taken off with price points around US$300. This also contains traditional Bluetooth headsets, although that market is in decline.

Although the technology for making wireless headsets and earbuds has been around for almost a decade, consumer acceptance has been slow to emerge. The core standard – the Bluetooth Advanced Audio Distribution Profile (A2DP) was released in 2006 and wireless headsets became available soon afterwards, along with support on mobile phones. Despite this, it was not until the end of 2014 that the market for wireless stereo headsets started to take off. It is still unclear what prompted this sudden change. The most credible explanation is the rise in mobile video. Unlike music consumption, where the user only needs to interact with their phone or music source at the end of a song or album, allowing them to keep the audio source in their pocket, watching mobile video requires a user to hold their screen. Whether that’s a tablet or phone, the cable becomes far more problematic when you’re holding the device in front of you. Whatever the reason, high end wireless headset manufacturers uniformly reported demand exceeding supply in the Christmas 2014 period, and have seen continuing enhanced levels of sales.

The second segment of the market is hearing aids, a largely unseen market, despite its US$14 billion annual turnover. Dominated by six companies, the industry has developed some very advanced processing and packaging technologies and is now embracing wireless connectivity to iPhones, as well as driving a future Bluetooth audio standard which will lead to a new generation of hearing aids that connect to most audio sources.

Where the big opportunity comes for hearable devices is in bridging the gap between these two segments, and potentially cannibalizing much of what is happening on the wrist. Humanity’s relatively recent addiction to music and particularly loud music is leading to a major future problem.

Hearing loss is set to be the new diabetes. In a recent report the World Health Organization (WHO) estimated that around 1.1 billion young people under the age of 30 are at serious risk of hearing loss because of their levels of sound exposure.

Although not as medically debilitating as diabetes, the prospect of billions of people having hearing difficulties when they still have thirty years of working life will have profound effects both in the workplace and society in general.

Whilst one view is that this generates an opportunity for the current hearing aid industry, they have not shown any indication that they will change their business model. Currently, hearing aid manufacturers ring-?fence their market by classifying their products as medical devices, selling them through qualified audiologists or health services. This has the dual feature of keeping prices high and divorcing the consumer from making purchase decisions based on their features. Although it is a route to market which has largely preserved or even increased the product cost, it has also slowed the pace of innovation and consumer demand. A number of companies have entered the market with lower cost devices, differentiating these as Assisted Listening Devices to circumvent the medical approval process. Historically the extent of innovation in these has been limited, confining them to local markets, and making little difference to the main market.

The Onset of Disruption

The status quo of hearables has been largely unchanged for many years. Three different industries have been putting electronics into people ears:

- Hearing aid manufacturers

- Wireless stereo headset manufacturers

- Bluetooth headset manufacturers

With few exceptions, there has been little crossover between these different areas – each one taking a different technical path. In 2013 that started to change. Two disruptive events happened. The first was that Apple took the initiative to add support for hearing aids in its MFI program, developing a proprietary extension to Bluetooth Smart and licensing it to two hearing aid vendors. It was the first step in connecting the hearing aid and consumer electronics industries, offering the user the ability to listen to phone calls as well as stream music. That persuaded the hearing aid industry to initiate a non-?proprietary standard for low power Bluetooth audio, which is currently progressing through the Bluetooth SIG. When complete it will not only provide audio streaming to hearing aids, but also enable a new generation of stereo headsets with significantly longer battery life.

The second disruption was the availability of a new generation of lower power Bluetooth chips that added functionality to enable the design of wireless earbuds. Before this, it had not been feasible to send audio separately to left and right ears, resulting in designs all taking the form of conventional stereo headsets. The new chips made it possible to design individual earbuds with no cable connection between them. In addition they also supported Bluetooth Low Energy, allowing manufacturers to pull information back from sensors within the earbuds.

For many years it had been known that the ear provided a good site for many health sensors, but accessing these through a cable had been impracticable. The opportunity to use a wireless connection opened up a new set of product possibilities, which had the potential to usurp the wrist as the best place for sensing.

The first company to latch onto these capabilities and announce a product was Bragi of Munich, who launched their Dash earbuds on Kickstarter, raising an impressive US$3.39 million. Their earbuds contain a wide range of sensors, aiming the product at the sports niche, where they can provide feedback to help improve or encourage the athlete. They have hit technology challenges but started shipping in January 2016.

Many others have followed. Within the crowdfunding sphere, there have been over fifteen hearables projects that have been successfully funded, to the tune of almost US$12 million. There is obviously public demand.

To date, almost all of these have fallen either in the category of stereo headsets with advanced control or content management, or earbuds aimed at the sports and fitness niche. An interesting, recent outlier is the Here from Doppler Labs, which provides attenuation or adjustment of ambient sound. Despite Doppler Lab’s earlier Dubs earplugs, which were firmly targeted at protection, the Here takes the view that there is a market to “curate” sound. That is a very individual approach.

All of these products chip away at the edges of convergence between music, health, hearing protection and hearing aid. So far none have publicly gone for the holy grail of full convergence, supporting today’s user’s evolution of hearing, which encompasses music streaming, protection and the transition to assisted listening. To achieve that is challenging, but it offers by far the largest market opportunity.

There is a further driver on the horizon, which should help drive the hearables market. That’s the growing use of voice recognition as a method of control. Google, Apple and Microsoft have all introduced voice recognition for their smartphone platforms and are in the process of rolling that out to other devices. Apple’s Homekit already enables voice control of major smart home functions. Over the next few years, voice control is likely to reduce the user’s dependence on their smartphone, or at least remove the direct manual interaction with it. However, that needs users to wear a microphone in some sort of wearable device. Wireless earbuds would seem to be the most likely place for that to happen. So the companies which make their mark in hearables will be in prime position to be the point of control for their environment. After a decade of touching and looking, the human voice could once more become dominant in communication.

Business Models

All wearable devices are challenged by the business model, particularly where they require an ongoing service, as do the myriad of fitness devices, where suppliers need to provide constantly updated apps. In contrast, hearables sit in a sweet spot, as their initial use cases largely consume the same audio streaming services of existing wired audio products. That means they can scale immediately. As sensors develop, new services can be layered on top, potentially based on what a user actually hears. However, the user delight and acceptance does not demand new applications, just enhanced performance.

The key requirements here are understanding comfort (fit in the ear), audio processing to “improve” the acoustic environment with noise cancellation and sound enhancements and finally, battery life.

They also need to be fashionable, as hearables will not succeed if the public continues to see them as just hearing aids.

It’s a set of skills which are uncommon. Some sit within the hearing aid industry, but others lie outside the medical environment and supply chain into which that industry has locked itself. As a result, disruption is most likely to come from companies with experience in this market, but a wider understanding of where consumers are going.

Making these devices is not simple, as all of the crowdfunded projects have discovered. Most of the component features are challenging, from wireless to miniaturization to battery life and power consumption. These are challenges which suggest we will see most success from companies with prior experience in these areas, not naive startups with no background in the industry.

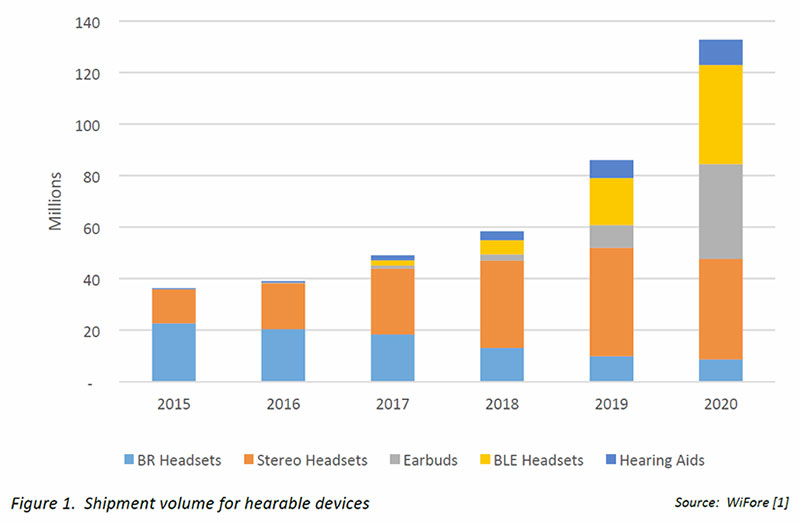

Market Size for Hearable Devices

Currently the hearables market is in transition. The original backbone – the Bluetooth headset, is seeing sales fall, due to higher integration of car kits. In contrast, wireless stereo headsets are taking off, probably spurred by a rise in mobile video. Wireless is also coming to the gaming headset, although that may have challenges in the short term with audio latency over the wireless link. That’s a soluble problem, as more modern codecs start to appear in wireless devices. In the longer term gaming may move into Augmented Reality headsets and goggles, moving out of the basic hearables market. That’s an even more difficult trend to predict.

The hearing aid industry is also changing. The advent of iPhone connectivity has lifted sales by around 30%, probably largely due to a removal of the stigma, as users are more prepared to accept a hearing aid with an associated Apple brand. That’s good news for the industry as a whole.

Wireless earbuds are only now arriving on the market. It’s difficult to predict how well the first few will perform and how soon the market will grow. If well received, it could be explosive. Existing consumer and hearing aid brands will almost certainly join in if they perceive it as successful, but will have to contend with extended development times to catch up. Existing hearing aids are optimized for sub-?miniature zinc air batteries. That means they are not easily re-purposed to support the new features of hearables. Other companies have a similarly long learning curve to understand the ear and the audio processing requirements. As a result, some of the early disrupters may well end up as acquisition targets.

When the new low power Bluetooth standard arrives, it will signal a second wave of innovation. That will extend battery life significantly, taking away some of the pain of charging, and as reference designs start to appear, will see the cost fall as product design becomes faster and easier. However, there will remain plenty of differentiators in terms of sensing to provide a healthy market for mid and high end manufacturers.

The medical side of hearing aids is well established, selling to health authorities and through audiologists where the products are subsidized by insurance. Models like that are remarkably robust to disruption in the short to medium term. So it is likely that these developments will initially grow the market for hearing aid companies as the stigma of wearing them starts to fall away. The big opportunity for new entrants is to establish their brand before hearing loss hits, at which point they can offer a progressive, lifetime solution for their users. That is likely to be a very profitable relationship.

Looking at these trends, the volume of hearable devices will grow sharply over the coming five years.

Stereo headsets will dominate in the short term, not least because they are already mature and growing in volume. By 2018 ear buds will become significant, as the initial problems are solved and the disruptive companies producing them start to move to scale. By 2019 some larger players will probably join the market, either directly or through acquisition.

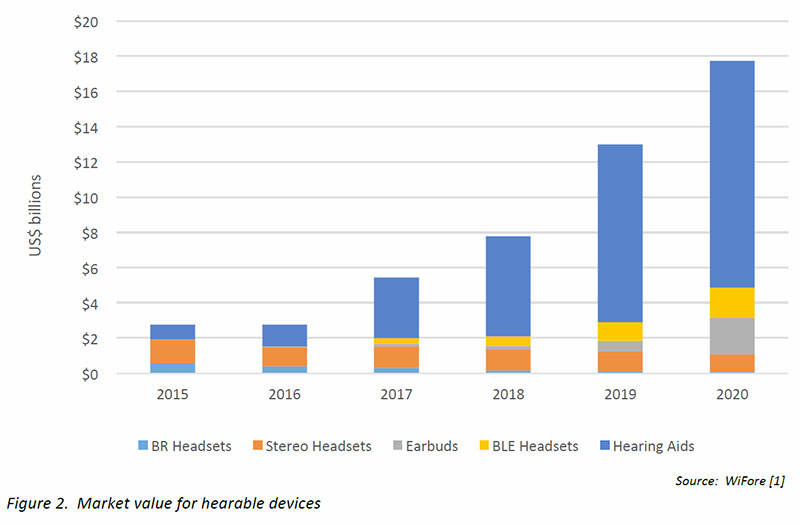

In terms of revenue, hearing aids, although one of the smaller volume segments, will dominate in terms of overall revenue, largely due to their historic sales and distribution channel which will maintain their high product price. The challenge will come from earbuds, which, if they gain customer acceptance will attract new users, not least from the 1.1 billion potential people identified by the WHO report as being susceptible to hearing loss. If they succeed, they will eventually take over the hearing aid category. These will be at a lower price, but with massively higher volumes.

A key challenge for disruption is to break the existing hearing aid supply chain, which means removing the need for the audiologist. Today the audiologist is the gate-keeper for hearing aids in most of the Western world. They have little interest in software or tools which would allow users to set up their own hearing aids, as that would threaten their business. However, the capabilities which are going into the new generation of hearables, along with phone apps and cloud analytics could perform as good a job for the majority of users with hearing loss. Several companies are already working on these tools, albeit mostly with existing hearing aids. Hearables companies that design their products with this capability will be in a strong position to disrupt the market. The trick is probably to make this an extension of everyday ambient sound curation. That allows users to buy the hearable as a consumer product and then check their hearing “because they can.”

If that works well, it provides a seamless journey into using it as an Assisted Listening Device, potentially ten years before they might consider having a hearing test for a hearing aid. Once won, the customer will probably never be lost.

Moreover, they are likely to update their device at a normal consumer replacement cycle, which is two or three time more frequently than that of a current hearing aid. If that happens, the potential for growth from 2020 onwards is enormous.

Even without challenging the hearing aid industry, the wireless ear bud will evolve into an important market in its own right. The projections for 2020 shipments only account for connections to around 0.5% of smartphones. Whilst the price point for hearables will never match that of wired earbuds, it will fall, making it an increasingly desirable option over time, with significant growth after 2020. As a result it will become one of the most successful areas within the wearables market.

Nick Hunn, WiFore Consulting

March 2016

About WiFore Consulting and author Nick Hunn

Nick Hunn is the founder and CTO of WiFore Consulting, which provides technology strategy, standards issues and product development to leading edge technology companies.

For the past thirty years Nick has been closely involved with short range wireless and communications, designing technology that helps to bring mobility to products, particularly in the areas of telematics, M2M, smart energy, wearables and mobile health. During that time he has started two high-?tech companies, both of which were acquired by multi-?national corporations. In the big data arena he has been involved in the roll out of connected home energy systems which have collected trillions of domestic energy readings, working with data scientists to analyze these streams of personal information and introduce the energy sector to big data. He is currently working on “appcessories” and hearable devices and chairs the Bluetooth Hearing Aid Working Group.

Nick has been closely involved with the Bluetooth SIG, the Continua Health Alliance, the ZigBee Alliance and other medical, smart energy and standards groups. He is the author of “The Essentials of Short Range Wireless” – a book attempting to explain the application of wireless technologies to product developers, and is currently writing a second book about the use of Bluetooth low energy for Appcessories, Wearables and the Internet of Things. Nick has an M.A. from Cambridge University and can be contacted at [email protected].